What Does Social Distancing Mean For Airlines?

What Does Social Distancing Mean For Airlines?

Its been great to see some positive announcements this week about restrictions lifting on travel. Woo hoo!

In Australia we have set some dates around the start-up of interstate travel coming back and for New Zealand, Level 2 Alert status came into effect yesterday and with it multiple new domestic routes on sale.

And while we still face a long road to full recovery, I think we are all in the mood for some positive moves! It is Friday 😊

This week I’ve had many chats with airports and tourism folks around what does this all mean for demand? And while airlines are adding back frequency (thank you!), what can we expect in regard to load factors and creeping back to pre-COVID passenger numbers?

A key consideration is what are the airlines in reality allowed to sell – how many seats onboard are available per flight?

Load factors won’t be operating at some of the high 80% full of pre-COVID levels. So for the fly market, even if we return to pre-COVID capacity, the flow on effect of social distancing will mean less passengers in airport terminals for the short term. That is unless we can add frequency!

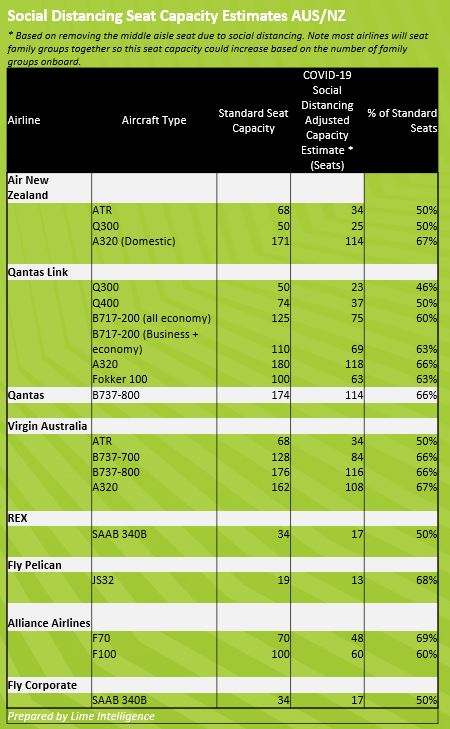

In an attempt to quantify what social distancing onboard means in one spot, I’ve pulled together the below table which estimates the number on seats by airline and aircraft type.

Logic used is based on:

- Airline advice around not selling middle row seats (I’ve estimated what removing these would mean for capacity);

- A caveat around these estimated capacity levels is that if large family groups or folks from the same household are travelling together then the number of seats sold would go up. Airlines have said they will aim to seat family together; and

- Every airline is treating the situation slightly differently so these estimates could change.

These are designed as a guide/estimate only to aid forecasting and it will be interesting to see how long these restrictions stay in play. Most folks agree its likely to remain until at least September.